Tax Value Of Pre Existing Carpet

Http Www Oregon Gov Dor Forms Formspubs Methods Valuing Personal Property 303 450 Pdf

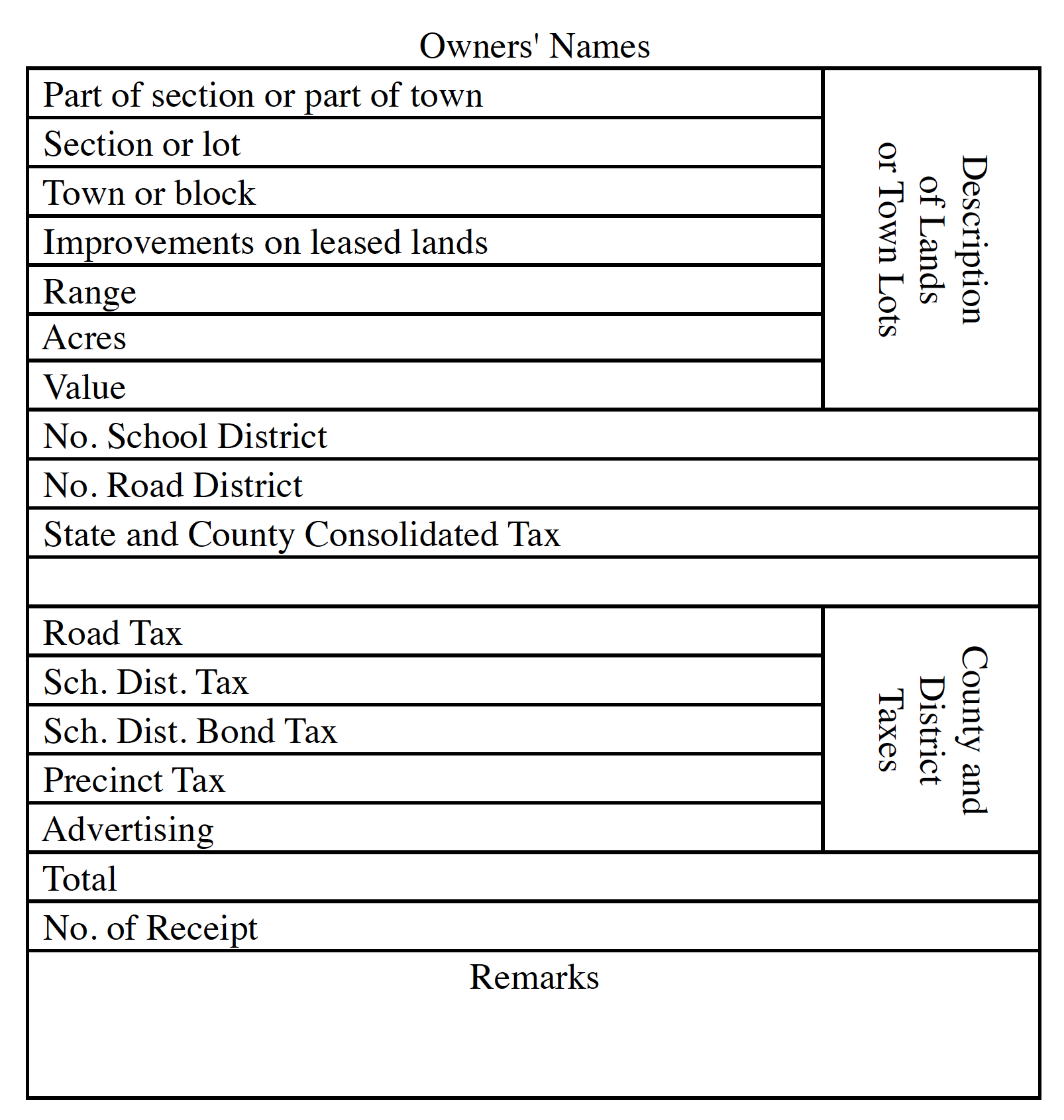

Chapter 77 Revenue And Taxation

Http Azdor Gov Sites Default Files Media Tpt 2015 Tpt For Contractors Post Sb1446 Handout2 Pdf

Https Www Floridarealtors Org Sites Default Files 2018 06 Florida Realtors Contract For Residential Sale And Purchase Crsp 15 Preparation Manual Released February 2018 0 Pdf

Http Www Mnesta Org Wp Content Uploads 2018 12 Contractors Fs128 Pdf

Https Docs Legis Wisconsin Gov Code Admin Code Tax 11 Pdf

Furthermore the draft regulations include relief provisions whereby pre existing entity accounts with account balances of 250 000 or less are exempt from review until the account balance exceeds 1 000 000 at the end of any calendar year.

Tax value of pre existing carpet.

Https Foundation Sdsu Edu Pdf Ap Sales Use Tax Guide Pdf

Https Www Mscpaonline Org Writable Committee Updates Document Repair V Capitalization Davidfabian Pdf

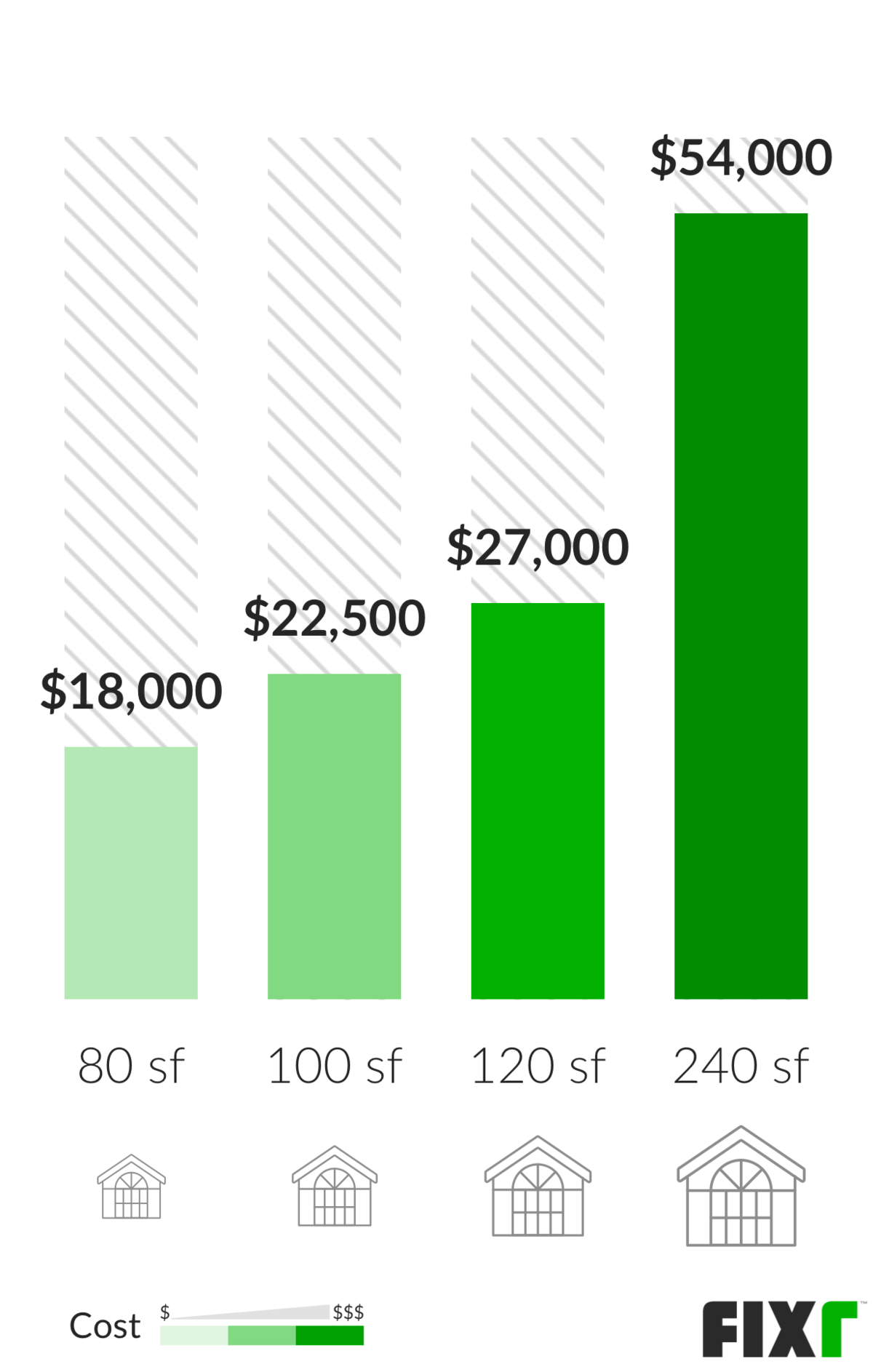

2020 Sunroom Addition Cost Cost To Build Sunroom

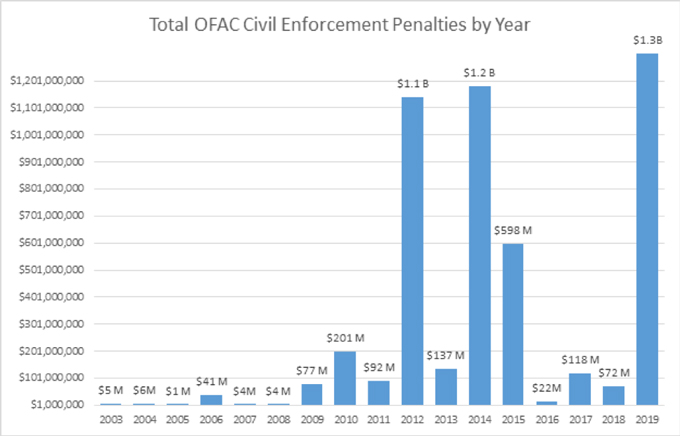

Gibson Dunn 2019 Year End Sanctions Update

Https Www Rd Usda Gov Files Hb 1 3550 Pdf

Https Sanjuancounty Colorado Gov Sites Sanjuancounty Files 2020 04 3 8 17 Land Use Code Searchable Compressed Pdf

Best Places To Buy Carpet Get Cheap Installation Homeadvisor

Flooring Installation Cost Per Sq Ft 2018 Urban Customs

2020 Lead Based Paint Removal Or Abatement Costs Homeadvisor

Stairway Remodel Part 1 Ripping Out Old Carpet And Finding Pressboard Plywood The Cookie Writer Staircase Remodel Diy Diy Stairs Staircase Remodel

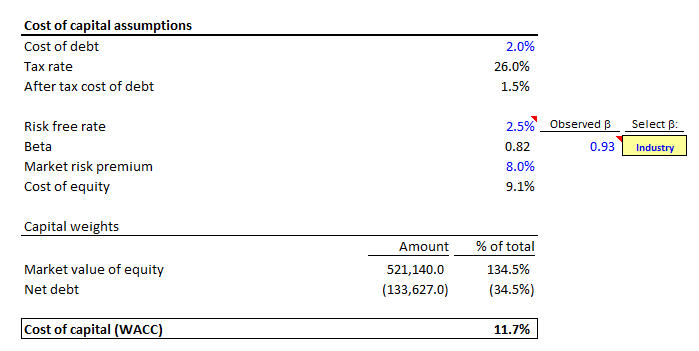

Wacc Formula Calculation Weighted Average Cost Of Capital Wall Street Prep

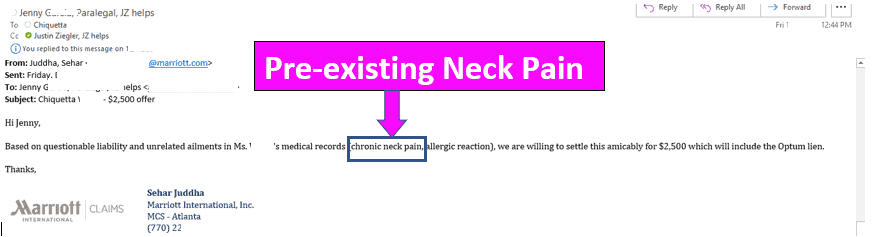

Hotel Injury Cases And Settlements In 2020 Accidents And Negligence

Https S3 Us West 2 Amazonaws Com Oerfiles Microeconomics Microeconomics 7 2 18 Pdf

How Much Does It Cost To Renovate A House A Guide For Real Estate Investors Lendinghome Blog

Https Www Elfaonline Org Docs Default Source Industry Topics Accounting Ey Us Leaseaccounting 16january2017 Pdf Sfvrsn Deb6d20d 0

Https Www Irem Org File 20library Globalnavigation Learning Courses Managementplanhandbook Pdf

2020 Home Elevator Cost Residential Lift Installation Price Homeadvisor

What Could Possibly Go Wrong On Your Refinance Appraisal Mortgage Blog

1

Sentryhome Flea Free Breeze Home And Carpet Spray 24 Fl Oz Petco

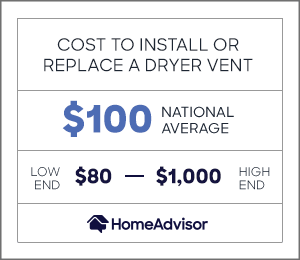

2020 Cost To Install Dryer Vent Replace Or Reroute Duct Hose Homeadvisor

Https Www Uaahq Org Uploads 1 2 6 6 126637856 Landlord Guide 2020 Final Pdf

Basement Flooring Options Basement Flooring Ideas

5 Pitfalls Of Buying A New Construction Home Millionacres

Source : pinterest.com